There are no guarantees in the world of investing… or are there? Here are six things I’m certain will happen in 2025.

1. There will be something huge to worry about in the financial markets.

Peter Lynch is the legendary manager of the Fidelity Magellan Fund who earned a 29% annual return during his 13-year tenure from 1977 to 1990. He once said:

“There is always something to worry about. Avoid weekend thinking and ignore the latest dire predictions of the newscasters. Sell a stock because the company’s fundamentals deteriorate, not because the sky is falling.”

Imagine a year in which all the following happened: (1) The US enters a recession; (2) the US goes to war in the Middle East; and (3) the price of oil doubles in three months. Scary? Well, there’s no need to imagine: They all happened in 1990. And what about the S&P 500? It has increased by more than 1,600% from the start of 1990 to today, even without counting dividends.

There will always be things to worry about. But that doesn’t mean we shouldn’t invest.

2. Individual stocks will be volatile.

From 1997 to today, the maximum peak-to-trough decline in each year for Amazon.com’s stock price ranged from 12.6% to 83.0%. In other words, Amazon’s stock price had suffered a double-digit fall every single year for 27 years. Meanwhile, the same Amazon stock price had climbed by an astonishing 233,924% (from US$0.098 to more than US$229) over the same period.

If you’re investing in individual stocks, be prepared for a wild ride. Volatility is a feature of the stock market – it’s not a sign that things are broken.

3. US-China relations will either remain status quo, intensify, or blow over.

“Seriously!?” I can hear your thoughts. But I’m stating the obvious for a good reason: We should not let our views on geopolitical events dictate our investment actions. Don’t just take my words for it. Warren Buffett himself said so. In his 1994 Berkshire Hathaway shareholders’ letter, Buffett wrote (emphases are mine):

“We will continue to ignore political and economic forecasts, which are an expensive distraction for many investors and businessmen.

Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.

But, surprise – none of these blockbuster events made the slightest dent in Ben Graham’s investment principles. Nor did they render unsound the negotiated purchases of fine businesses at sensible prices.

Imagine the cost to us, then, if we had let a fear of unknowns cause us to defer or alter the deployment of capital. Indeed, we have usually made our best purchases when apprehensions about some macro event were at a peak. Fear is the foe of the faddist, but the friend of the fundamentalist.

A different set of major shocks is sure to occur in the next 30 years. We will neither try to predict these nor to profit from them. If we can identify businesses similar to those we have purchased in the past, external surprises will have little effect on our long-term results.”

From 1994 to the third quarter of 2024, Berkshire Hathaway’s book value per share, a proxy for the company’s intrinsic value – albeit a flawed measure – grew by 13.5% annually. Buffett’s disciplined focus on long-term business fundamentals – while ignoring the distractions of political and economic forecasts – has worked out just fine.

4. Interest rates will move in one of three ways: Sideways, up, or down.

“Again, Captain Obvious!?” Please bear with me. There is a good reason why I’m stating the obvious again.

Much ado has been made about what central banks have been doing, and would do, with their respective economies’ benchmark interest rates. This is because of the theoretical link between interest rates and stock prices.

Stocks and other asset classes (bonds, cash, real estate etc.) are constantly competing for capital. In theory, when interest rates are high, the valuation of stocks should be low, since the alternative to stocks – bonds – are providing a good return. On the other hand, when interest rates are low, the valuation of stocks should be high, since the alternative – again, bonds – are providing a poor return.

But what does reality say? Here’re important historical data on the actual relationship between interest rates and stocks in the US:

- Rising interest rates have been met with rising valuations. According to data from economist and Nobel Laureate Robert Shiller, the US 10-year Treasury yield was 2.3% at the start of 1950. By September 1981, it had risen to 15.3%, the highest rate recorded in Shiller’s dataset. In that same period, the S&P 500’s price-to-earnings (P/E) ratio moved from 7 to 8. In other words, the P/E ratio for the S&P 500 increased slightly despite the huge jump in interest rates. It’s worth noting too that the S&P 500’s P/E ratio of 7 at the start of 1950 was not a result of earnings that were temporarily inflated. Yes, there’s cherry picking with the dates. For example, if I had chosen January 1946 as the starting point, when the US 10-year Treasury yield was 2.2% and the P/E ratio for the S&P 500 was 19, then it would be a case of valuations falling alongside rising interest rates. But this goes to show that while interest rates have a role to play in the movement of stocks, it is far from the only thing that matters.

- Stocks have climbed in rising interest rate environments. In a September 2022 piece, Ben Carlson, Director of Institutional Asset Management at Ritholtz Wealth Management, showed that the S&P 500 climbed by 21% annually from 1954 to 1964 even when the yield on 3-month Treasury bills (a good proxy for the Fed Funds rate, which is the key interest rate set by the Federal Reserve) surged from around 1.2% to 4.4% in the same period. In the 1960s, the yield on the 3-month Treasury bill doubled from just over 4% to 8%, but US stocks still rose by 7.7% per year. And then in the 1970s, rates climbed from 8% to 12% and the S&P 500 still produced an annual return of nearly 6%.

- Stocks have done poorly in both high and low interest rate environments, and have also done well in both high and low interest rate environments. Carlson published an article in February 2023 that looked at how the US stock market performed in different interest rate regimes. It turns out there’s no clear link between the two. In the 1950s, the 3-month Treasury bill (which is effectively a risk-free investment, since it’s a US government bond with one of the shortest maturities around) had a low average yield of 2.0%; US stocks returned 19.5% annually back then, a phenomenal gain. In the 2000s, US stocks fell by 1.0% per year when the average yield on the 3-month Treasury bill was 2.7%. Meanwhile, a blockbuster 17.3% annualised return in US stocks in the 1980s was accompanied by a high average yield of 8.8% for the 3-month Treasury bill. In the 1970s, the 3-month Treasury bill yielded a high average of 6.3% while US stocks returned just 5.9% per year.

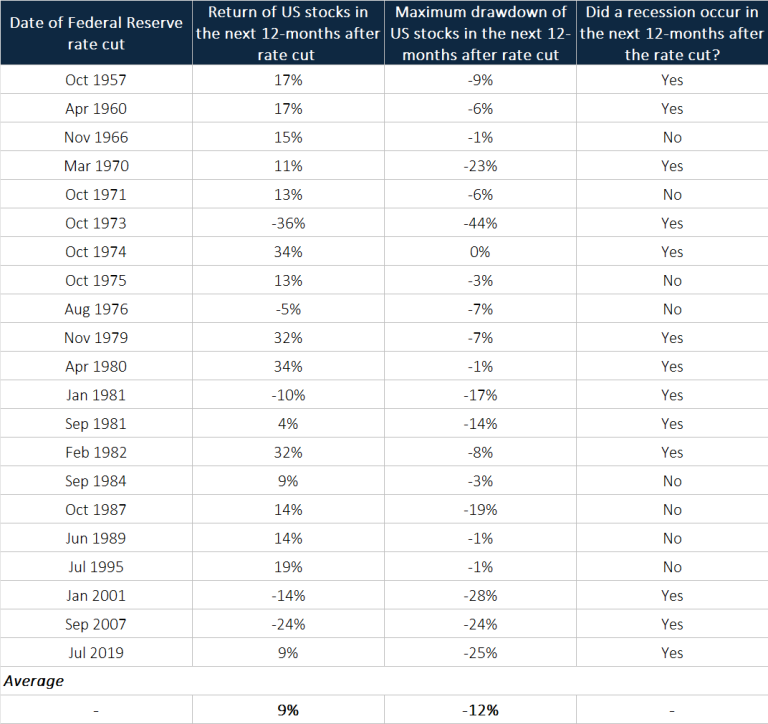

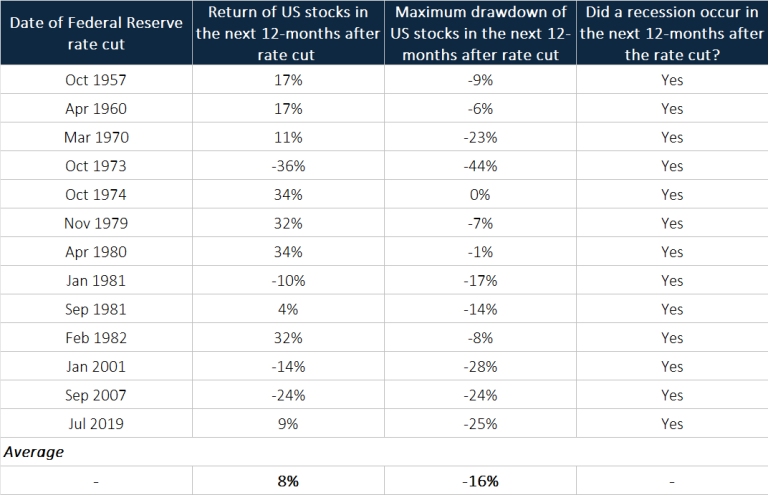

- A cut in interest rates by the Federal Reserve is not guaranteed to be a good or bad event for stocks. Josh Brown, CEO of Ritholtz Wealth Management, shared fantastic data in an August 2024 article on how US stocks have performed in the past when the Federal Reserve lowered interest rates. His data, in the form of a chart, goes back to 1957 and I reproduced them in tabular format in Table 1; it shows how US stocks did in the next 12 months following a rate cut, as well as whether a recession occurred in the same window. I also split the data in Table 1 according to whether a recession had occurred shortly after a rate cut, since eight of the 21 past rate-cut cycles from the Federal Reserve since 1957 took place without an impending recession. Table 2 shows the same data as Table 1 but for rate cuts with a recession; Table 3 is for rate cuts without a recession. What the data show is that US stocks have historically done well, on average, in the 12 months following a rate-cut. The overall record, seen in Table 1, is an average 12-month forward return of 9%. When a recession happened shortly after a rate-cut, the average 12-month forward return is 8%; when a recession did not happen shortly after a rate-cut, the average 12-month forward return is 12%. A recession is not necessarily bad for stocks. As Table 2 shows, US stocks have historically delivered an average return of 8% over the next 12 months after rate cuts that came with impending recessions. It’s not a guarantee that stocks will produce good returns in the 12 months after a rate cut even if a recession does not occur, as can be seen from the August 1976 episode in Table 3.

It turns out that the actual relationship between interest rates and stocks is not as clear-cut as theory suggests. There’s an important lesson here, in that one-factor analysis in finance – “if A happens, then B will occur” – should be largely avoided because clear-cut relationships are rarely seen.

I also think that time that’s spent watching central banks’ decisions regarding interest rates will be better spent studying business fundamentals. The quality of a company’s business and the growth opportunities it has matter far more to its stock price over the long run than interest rates.

Sears is a case in point. In the 1980s, the US-based company was the dominant retailer in the country. Morgan Housel wrote in a blog post, Common Plots of Economic History :

“Sears was the largest retailer in the world, housed in the tallest building in the world, employing one of the largest workforces.

“No one has to tell you you’ve come to the right place. The look of merchandising authority is complete and unmistakable,” The New York Times wrote of Sears in 1983.

Sears was so good at retailing that in the 1970s and ‘80s it ventured into other areas, like finance. It owned Allstate Insurance, Discover credit card, the Dean Witter brokerage for your stocks and Coldwell Banker brokerage for your house.”

US long-term interest rates fell dramatically from around 15% in the early-to-mid 1980s to around 3% in 2018. But Sears filed for bankruptcy in October 2018, leaving its shareholders with an empty bag. In his blog post mentioned earlier, Housel also wrote:

“Growing income inequality pushed consumers to either bargain or luxury goods, leaving Sears in the shrinking middle. Competition from Wal-Mart and Target – younger and hungrier – took off.

By the late 2000s Sears was a shell of its former self. “YES, WE ARE OPEN” a sign outside my local Sears read – a reminder to customers who had all but written it off.”

If you’re investing for the long run, there are far more important things to watch than interest rates.

5. There will be investors who are itching to make wholesale changes to their investment portfolios for 2025.

Ofer Azar is a behavioural economist. He once studied more than 300 penalty kicks in professional football (or soccer) games. The goalkeepers who jumped left made a save 14.2% of the time while those who jumped right had a 12.6% success rate. Those who stayed in the centre of the goal saved a penalty 33.3% of the time.

Interestingly, only 6% of the keepers whom Azar studied chose to stay put in the centre. Azar concluded that the keepers’ moves highlight the action bias in us, where we think doing something is better than doing nothing.

The bias can manifest in investing too, where we develop the urge to do something to our portfolios, especially during periods of volatility. We should guard against the action bias. This is because doing nothing to our portfolios is often better than doing something. I have two great examples.

First is a paper published by finance professors Brad Barber and Terry Odean in 2000. They analysed the trading records of more than 66,000 US households over a five-year period from 1991 to 1996. They found out that the most frequent traders generated the lowest returns – and the difference is stark. The average household earned 16.4% per year for the timeframe under study but the active traders only made 11.4% per year.

Second, finance professor Jeremy Siegel discovered something fascinating in the mid-2000s. In an interview with Wharton, Siegel said:

“If you bought the original S&P 500 stocks, and held them until today—simple buy and hold, reinvesting dividends—you outpaced the S&P 500 index itself, which adds about 20 new stocks every year and has added almost 1,000 new stocks since its inception in 1957.”

Doing nothing beats doing something.

6. There are nearly 8.2 billion individuals in the world today, and the vast majority of us will wake up every morning wanting to improve the world and our own lot in life.

This motivation is ultimately what fuels the global economy and financial markets. There are miscreants who appear occasionally to mess things up, but we should have faith in the collective positivity of humankind. We should have faith in us. The idiots’ mess will be temporary.

Mother Nature threw us a major global health threat in 2020 with COVID-19. But we – mankind – managed to build a vaccine against the disease in record time; Moderna even managed to design its vaccine in just two days. This is a great example of the ingenuity of humanity at work.

To me, investing in stocks is the same as having the long-term view that we humans are always striving, collectively, to improve the world.

A final word

This article is a little cheeky, because it describes incredibly obvious things, such as “interest rates will move in one of three ways: sideways, up, or down.” But I wrote it in the way I did for a good reason. A lot of seemingly important things in finance – things with outcomes that financial market participants obsess over and try to predict – actually turn out to be mostly inconsequential for long-term investors. Keep this in mind when you read the next “X Things That Will Happen To Stocks in 2025” article.

Disclaimer: The Good Investors is the personal investing blog of two simple guys who are passionate about educating Singaporeans about stock market investing. By using this Site, you specifically agree that none of the information provided constitutes financial, investment, or other professional advice. It is only intended to provide education. Speak with a professional before making important decisions about your money, your professional life, or even your personal life. I currently have a vested interest in Amazon. Holdings are subject to change at any time.