From what I see, most investors are often on the lookout for ways to win in the stock market. But that may be the wrong focus, as economist Erik Falkenstein writes:

“In expert tennis, 80% of the points are won, while in amateur tennis, 80% are lost. The same is true for wrestling, chess, and investing: Beginners should focus on avoiding mistakes, experts on making great moves.”

In keeping with the spirit of Falkenstein’s thinking, here are some big investing blunders to avoid.

1. Not realising how common volatility is even with the stock market’s biggest long-term winners

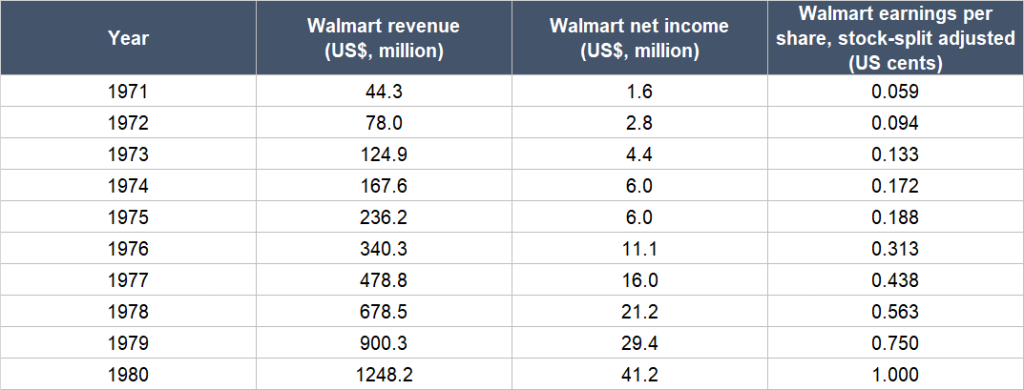

From 1971 to 1980, the American retailer Walmart produced breath-taking business growth. Table 1 below shows the near 30x increase in Walmart’s revenue and the 1,600% jump in earnings per share in that period. Unfortunately, this exceptional growth did not help with Walmart’s short-term return.

Based on the earliest data I could find, Walmart’s stock price fell by three-quarters from less than US$0.04 in late-August 1972 to around US$0.01 by December 1974 – in comparison, the US stock market, represented by the S&P 500, was down by ‘only’ 40%.

Table 1; Source: Walmart annual reports

But by the end of 1979, Walmart’s stock price was above US$0.08, more than double what it was in late-August 1972. Still, the 2x-plus increase in Walmart’s stock price was far below the huge increase in earnings per share the company generated.

This is where the passage of time helped – as more years passed, the weighing machine clicked into gear (I’m borrowing from Ben Graham’s brilliant analogy of the stock market being a voting machine in the short run but a weighing machine in the long run). At the end of 1989, Walmart’s stock price was around US$3.70, representing an annualised growth rate in the region of 32% from August 1972; from 1971 to 1989, Walmart’s revenue and earnings per share grew by 41% and 38% per year. Even by the end of 1982, Walmart’s stock price was already US$0.48, up more than 10 times where it was in late-August 1972.

Volatility is a common thing in the stock market. It does not necessarily mean that anything is broken.

2. Mixing investing with economics

China’s GDP (gross domestic product) grew by an astonishing 13.3% annually from US$427 billion in 1992 to US$18 trillion in 2022. But a dollar invested in the MSCI China Index – a collection of large and mid-sized companies in the country – in late-1992 would have still been roughly a dollar as of October 2022, as shown in Figure 1.

Put another way, Chinese stocks stayed flat for 30 years despite a massive macroeconomic tailwind (the 13.3% annualised growth in GDP).

Figure 1; Source: Duncan Lamont

Why have the stock prices of Chinese companies behaved the way they did? It turns out that the earnings per share of the MSCI China Index was basically flat from 1995 to 2021.

Figure 2; Source: Eugene Ng

Economic trends and investing results can at times be worlds apart. The gap exists because there can be a huge difference between a company’s business performance and the trend – and what ultimately matters to a company’s stock price, is its business performance.

3. Anchoring on past stock prices

A 2014 study by JP Morgan showed that 40% of all stocks in the Russell 3000 index in the US from 1980 to 2014 suffered a permanent decline of 70% or more from their peak values.

There are stocks that fall hard – and then stay there. Thinking that a stock will return to a particular price just because it had once been there can be a terrible mistake to make.

4. Think a stock is cheap based on superficial valuation metrics

My friend Chin Hui Leong from The Smart Investors had suffered through this mistake before and he has graciously shared his experience for the sake of letting others learn. In an April 2020 article, he wrote:

“The other company I bought in May 2009, American Oriental Bioengineering, has shrunk to such a tiny figure, making it a total loss…

…In contrast, American Oriental Bioengineering’s revenue fell from around $300 million in 2009 to about US$120 million by 2013. The company also recorded a huge loss of US$91 million in 2013…

…Case in point: when I bought American Oriental Bioengineering, the stock was only trading at seven times its earnings. And yet, the low valuation did not yield a good outcome in the end.”

Superficial valuation metrics can’t really tell us if a stock’s a bargain or not. Ultimately, it’s the business which matters.

5. Not investing due to fears of a recession

Many investors I’ve spoken to prefer to hold off investing in stocks if they fear a recession is around the corner, and jump back in only when the coast is clear. This is a mistake.

According to data from Michael Batnick, the Director of Research at Ritholtz Wealth Management, a dollar invested in US stocks at the start of 1980 would be worth north of $78 around the end of 2018 if you had simply held the stocks and did nothing. But if you invested the same dollar in US stocks at the start of 1980 and expertly side-stepped the ensuing recessions to perfection, you would have less than $32 at the same endpoint.

Said another way, history’s verdict is that avoiding recessions flawlessly would cause serious harm to your investment returns.

6. Following big investors blindly

Morgan Housel is currently a partner with the venture capital firm Collaborative Fund. Prior to this, he was a writer for The Motley Fool for many years. Here’s what Housel wrote in a 2014 article for the Fool (emphasis is mine):

“I made my worst investment seven years ago.

The housing market was crumbling, and a smart value investor I idolized began purchasing shares in a small, battered specialty lender. I didn’t know anything about the company, but I followed him anyway, buying shares myself. It became my largest holding — which was unfortunate when the company went bankrupt less than a year later.

Only later did I learn the full story. As part of his investment, the guru I followed also controlled a large portion of the company’s debt and and preferred stock, purchased at special terms that effectively gave him control over its assets when it went out of business. The company’s stock also made up one-fifth the weighting in his portfolio as it did in mine. I lost everything. He made a decent investment.”

We may never be able to know what a famous investor’s true motives are for making any particular investment. And for that reason, it’s important to never follow anyone blindly into the stock market.

7. Not recognising how powerful simple, common-sense financial advice can be

Robert Weinberg is an expert on cancer research from the Massachusetts Institute of Technology. In the documentary The Emperor of All Maladies, Weinberg said (emphases are mine):

“If you don’t get cancer, you’re not going to die from it. That’s a simple truth that we [doctors and medical researchers] sometimes overlook because it’s intellectually not very stimulating and exciting.

Persuading somebody to quit smoking is a psychological exercise. It has nothing to do with molecules and genes and cells, and so people like me are essentially uninterested in it — in spite of the fact that stopping people from smoking will have vastly more effect on cancer mortality than anything I could hope to do in my own lifetime.”

I think Weinberg’s lesson can be analogised to investing. Ben Carlson is the Director of Institutional Asset Management at Ritholtz Wealth Management. In a 2017 blog post, Carlson compared the long-term returns of US college endowment funds against a simple portfolio he called the Bogle Model.

The Bogle Model was named after the late index fund legend John Bogle. It consisted of three, simple, low-cost Vanguard funds that track US stocks, stocks outside of the US, and bonds. In the Bogle Model, the funds were held in these weightings: 40% for the US stocks fund, 20% for the international stocks fund, and 40% for the bonds fund. Meanwhile, the college endowment funds were dizzyingly complex, as Carlson describes:

“These funds are invested in venture capital, private equity, infrastructure, private real estate, timber, the best hedge funds money can buy; they have access to the best stock and bond fund managers; they use leverage; they invest in complicated derivatives; they use the biggest and most connected consultants…”

Over the 10 years ended 30 June 2016, the Bogle Model produced an annual return of 6.0%. But even the college endowment funds that belonged to the top-decile in terms of return only produced an annual gain of 5.4% on average. The simple Bogle Model had bested nearly all the fancy-pants college endowment funds in the US.

Simple advice can be very useful and powerful for many investors. But they’re sometimes ignored because they’re too simple, despite how effective they can be. Don’t make this mistake.

Disclaimer: The Good Investors is the personal investing blog of two simple guys who are passionate about educating Singaporeans about stock market investing. By using this Site, you specifically agree that none of the information provided constitutes financial, investment, or other professional advice. It is only intended to provide education. Speak with a professional before making important decisions about your money, your professional life, or even your personal life. I do not have a vested interest in any companies mentioned. Holdings are subject to change at any time.