Editor’s note: We’re testing out a new series for the blog, the “Company Notes Series”, where we periodically share our notes on companies we’ve studied in the recent past but currently have no vested interest in (we may invest in or sell shares in the companies mentioned at any time). The notes are raw and not updated, and the “as of” date for the data is given at the start of the notes. The first edition in the series can be found here. Please give us your thoughts on the series through the “Contact Us” page; your feedback will determine if we continue with it. Thanks in advance!

Start of notes for BayCurrent Consulting

Data as of 31 May 2023

Background

- Founded in March 1998 as PC Works Co. Ltd for the purpose of consulting, system integration and outsourcing related to management, operations and IT. In December 2006, PC Works Co. Ltd changed its name to BayCurrent Consulting Co. Ltd. In April 2014, Byron Holdings Co. Ltd was set up. In June 2014, Byron Holdings Co. Ltd acquired BayCurrent Consulting Co. Ltd and then the combined entity changed its name to BayCurrent Consulting Co. Ltd.

- HQ: Tokyo, Japan

- Listed on September 2016 on the Tokyo Stock Exchange Mother’s section; moved to First Section of Tokyo Stock Exchange on December 2018; moved to Prime Market of the Tokyo Stock Exchange on April 2022

- Ticker: TSE: 6532

- Total number of consultants as of FY2023 (financial year ended February 2023) is 2,961; total number of employees as of FY2023 is 3,310

Business

- BayCurrent is a consulting firm that supports a wide range of themes such as strategy, digital, and operations for Japan’s leading companies in various industries. BayCurrent provides planning and execution support to clients, such as company-wide strategy planning and business strategy planning to support decision-making by management, and support for examining business operations using digital technology.

- Examples of the projects that BayCurrent is currently working on under Digital Consulting:

- Finance, Cashless payment, and Design: Building a UX improvement process to continue achieving high customer satisfaction over the long term

- Pharmaceutical manufacturing, Digital technologies, and Market research: Formulating plans to enter the Japanese market of advanced digital medical equipment business for foreign companies

- Telecommunication, Metaverse, and Business planning: Developing plans to use metaverse and examine the use of AI toward the smart city concept

- Automobiles, AI, and Business creation: Building a model for business using AI and supporting its implementation, aiming to reduce the risk of traffic accidents

- Examples of the projects that BayCurrent is currently working on under Sustainability Consulting:

- Energy, ESG, and Support for practice: Forming a scheme and supporting negotiations for realizing offshore wind power business

- Finance and Carbon neutrality: Considering policies in response to TCFD (Task Force on Climate-Related Financial Disclosures) in anticipation of sales of solutions in the future

- High-tech, EV, and Business planning: Considering business domains and creating a road map for popularizing EVs (electric vehicles) to reduce CO2 emissions

- Manufacturing, ESG, and Supply chain management: Considering the possibility of commercializing supplier ESG assessments and risk management

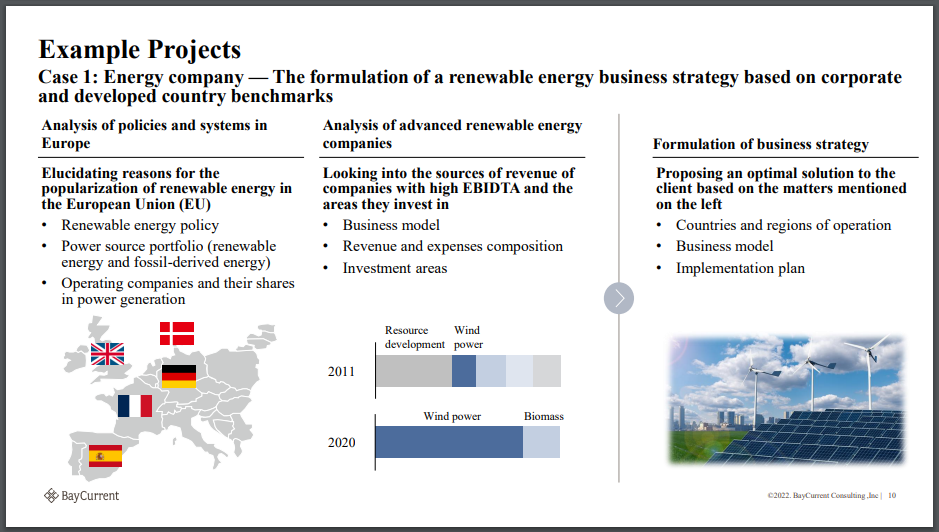

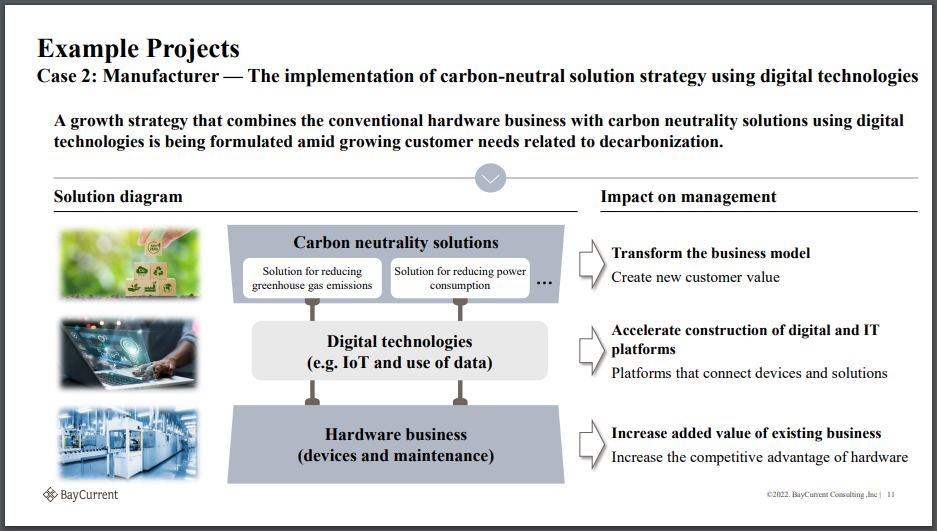

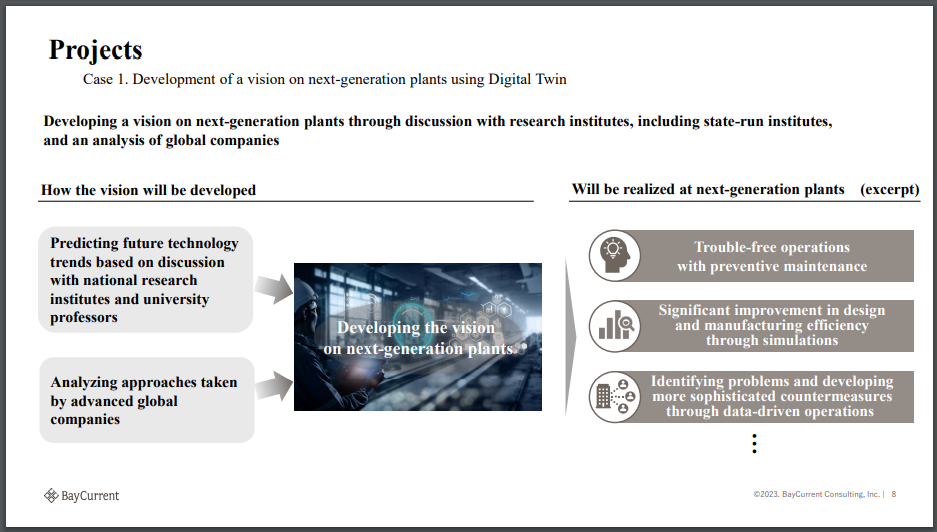

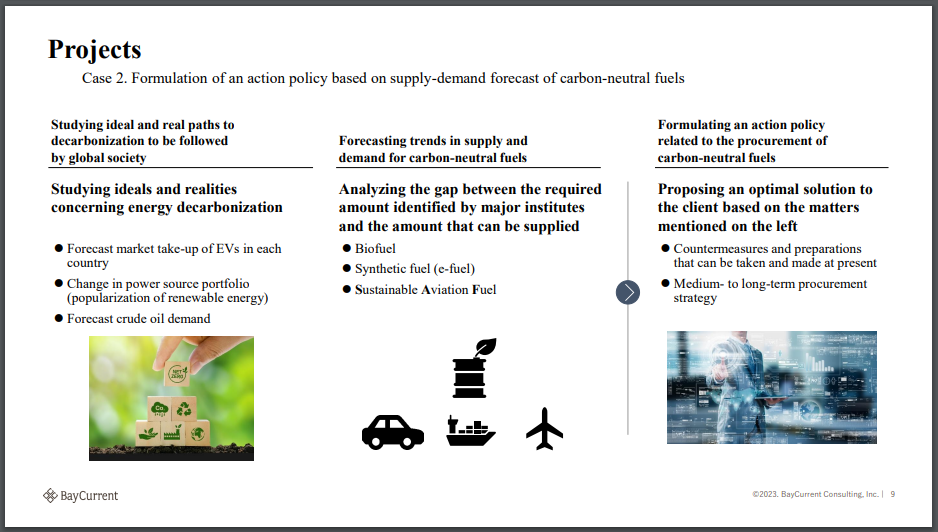

- See also Figures 1, 2, 3, and 4 for examples of BayCurrent’s projects

- BayCurrent groups its customers into three industry categories: Finance (banking, securities, insurance etc); Telecommunications/Media/High-Tech; and Others (energy, entertainment, government offices, food etc). In FY2023, 25% of revenue was from Finance, 35% was from Telecommunications/Media/High-Tech, and 40% from Others. In FY2019, the split was 40% from Finance, 30% from Telecommunications/Media/High-Tech, and 30% from Others. BayCurrent’s largest customer in FY2023 was Pfizer Japan, accounting for 12.0% of revenue; it seems like there’s no other company that accounted for more than 10% of revenue during the year.

- In FY2023, revenue from customers based in Japan was at least 90% of BayCurrent’s total revenue.

Market opportunity

- According to IDC Japan’s “Forecast for domestic business consulting market: 2021-2025” (announced on 1 July 2021), the Japanese consulting market is expected to have a CAGR of 7.8% from around ¥900 billion in 2020 to more than ¥1.2 trillion in 2025; within the consulting market is the digital consulting sub-segment which is expected to have a CAGR of 30.1% from more than ¥100 billion in 2020 to around ¥500 billion in 2025. BayCurrent ended FY2023 with revenue of just ¥76.1 billion.

- According to BayCurrent: “In today’s business environment, the challenges faced by corporate managers are becoming more diverse and complex due to intensifying market competition and changes in market structure. There is a growing need for consultants with a high level of expertise. Furthermore, with the further development of digital technology in the future, the need for the utilization of new technologies in business is expected to increase year by year, and the consulting market is expected to continue to grow at a high rate.”

- In Japan, there’s an initiative called DX (Digital Transformation) that began to be promoted heavily by the Japanese government starting in 2018 with the publication of the “DX [Digital Transformation]” report by the Ministry of Economy, Trade, and Industry (METI) during the year. METI warned that Japan would face an economic loss of ¥12 trillion per year by 2025 if traditional mainframes and backbone core systems were not updated and the shortage of ICT engineers were not addressed. Moreover, in 2016, the percentage of companies that have been operating their core systems for 21 years or more is 20%, and 40% for companies that have been in operation for 11 to 20 year; if this situation continues in 10 years, in 2025, the percentage of companies that have been operating core systems for 21 years or more will be 60%. Japanese companies appear to have heeded the government’s DX call. Surveys conducted by the METI and FUJITSU in 2020 indicated that almost half of the SMEs were actively promoting DX companywide, while large companies with more than 5.000 employees indicate an adoption rate close to 80%. These are a tailwind for BayCurrent Consulting.

Growth strategy

- BayCurrent is focused on further increasing the added value of its consulting services; the recruitment and training of human resources; and providing an attractive work environment.

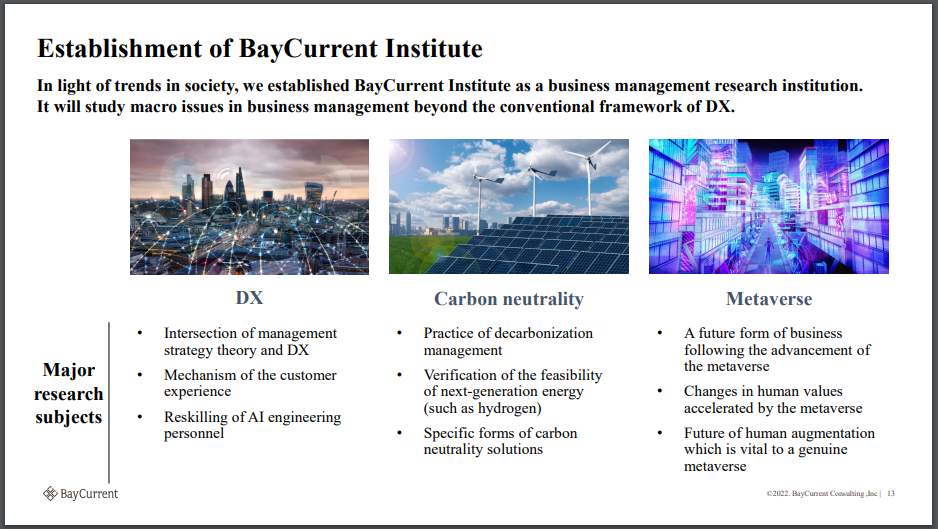

- BayCurrent’s support services for corporate managers in all industries are knowledge-intensive, and so management believes that improvements in the company’s consultants’ ability to make proposals and solve problems will affect its growth. For this reason, management strives to recruit excellent human resources with various backgrounds and focusing on creating an environment and treatment that makes it easy for each consultant to work with peace of mind. Management has established a wide variety of training programs and study sessions to improve its consultants’ skills for strategic planning and solving management issues. Management believes that BayCurrent is able to formulate viable strategies that meet the needs of clients precisely because the company’s consultants are professionals who have worked on numerous projects across industries and service areas; for this reason, management strives to not limit its consultants to specific fields. Figure 5 shows the establishment of the BayCurrent Institute, a business management research institute.

- Management also distributes knowledge obtained through dialogue with university professors working on research subjects and members of the management teams of leading companies, in order to gain visibility from the public. Most recent examples of such work:

- Participated in FIN/SUM, one of Japan’s largest fintech conferences, co-hosted by the Financial Services Agency and Nikkei Inc. BayCurrent did the following: Joji Noritake, Managing Executive Officer and CDO, conducted a standalone lecture on “Sustainable customer experience connects emotional memories”; took part in panel discussion on “Possibility of future individual investment through digital technology”

- Participation in Green CPS Consortium, an organization aimed at building eco-friendly industry and society by controlling material loss, energy loss, and other aspects in all economic activities while driving economic growth

- Made a donation to the VR/metaverse in the corporate sponsored practical research program of the University of Tokyo Virtual Reality Educational Research Center. The research program conducts basic research on the creation and operation of metaverse space and conducts demonstration experiments to develop practical applications of the metaverse in society.

- Growth of number of consultants vs growth of revenue (note the higher revenue growth vs consultant growth):

Financials

- Financials from FY2016 to FY2023 (financials in ¥; earliest data we could find was for FY2016):

- Solid CAGRs in revenue:

- FY2016-FY2023: 25.1%

- FY2018-FY2023: 30.1%

- FY2023: 32.4%

- Profitable since at least FY2016. Net income CAGRs and average net income margins:

- FY2016-FY2023: 52.3% CAGR, 15.3% average margin

- FY2018-FY2023: 60.3% CAGR, 18.1% average margin

- FY2023: 43.3% growth, 27.6% margin

- Positive operating cash flow since at least FY2016. Operating cash flow CAGRs and average operating cash flow margins:

- FY2016-FY2023: 34.0% CAGR, 19.4% average margin

- FY2018-FY2023: 45.0% CAGR, 21.6% average margin

- FY2023: 35.5% growth, 27.2% margin

- Free cash flow positive since at least FY2016. Free cash flow CAGRs and average free cash flow margins:

- FY2016-FY2023: 34.0% CAGR, 19.1% average margin

- FY2018-FY2023: 45.8% CAGR, 21.3% average margin

- FY2023: 33.6% growth, 26.7% margin

- Balance sheet was initial in net-debt position and became net-cash in FY2020 onwards; high net-cash position of ¥33 billion in FY2023

- Minimal dilution as weighted average diluted share count increased by only 0.8% per year for FY2016-FY2023, and -0.3% in FY2023

- Management aims for a total shareholder return ratio (dividends and share buybacks) of around 40% of earnings; dividend payout ratio is typically 20%-30% under IFRS. In FY2023, interim dividend of ¥14 per share (adjusting for 1-for-10 stock split in November 2022) and final dividend of ¥23 per share, for a total dividend of ¥37 per share for FY2023, representing a payout ratio of 27%.

Management

- Yoshiyuki Abe, 57, is President and CEO. Became President in December 2016. Joined the original BayCurrent Consulting Co. Ltd in September 2008 and became an executive director in November of same year. Yoshiyuki Abe became President in December 2016 after some major turmoil at BayCurrent that happened in H2 2016:

- Failed to gain deals matching waiting consultants and then suffered a largely lowered operation rate

- Additionally faced the defection of employees as a result of a talk about withdrawal that resulted in the loss of credibility of the clients receiving the support for many years

- Revised earnings forecasts downwardly on 9 December 2016; on the same day, the former President left office

- Kentaro Ikehira, 46, is Executive Vice President. Became Vice President in May 2021. Joined the original BayCurrent Consulting Co. Ltd in September 2007.

- Kosuke Nakamura, 41, is CFO. Became CFO in May 2021. Joined the original BayCurrent Consulting Co. Ltd in January 2007.

- Management has a long history of significantly beating their own mid-term growth projections. Examples:

- In FY2018 earnings presentation, a projection for FY2019-FY2021 was given where revenue was expected to have a CAGR of 15%-20%, ending at ¥32-35 billion. Actual FY2021 revenue was ¥42.8 billion.

- In FY2022 earnings presentation, a projection for FY2022-FY2026 was given where revenue was expected to have a CAGR of 20% to end at ¥100 billion and EBITDA was expected to end at ¥30 billion. Projection given for FY2024 was for revenue of ¥94.6 billion and EBITDA of ¥36 billion – so FY2026 medium-term projection could be achieved/beat by as early as FY2024

- Management has set a target of FY2029 revenue of ¥250 billion, which represents a 20% CAGR from FY2024’s projected revenue of ¥94.6 billion.

Compensation of Management

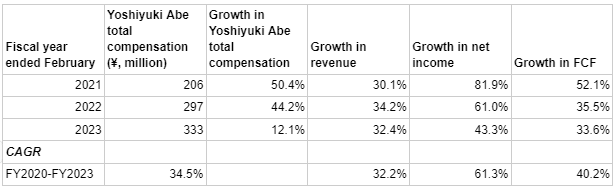

- Yoshiyuki Abe’s total FY2023 compensation was ¥333 million, consisting of ¥40 million of fixed pay, ¥192 million of performance-linked remuneration, and ¥101 million of restricted stock compensation. Total compensation in FY2023 was just 1.6% of FY2023 net income as well as free cash flow.

- Yoshiyuki Abe’s tota FY2022 compensation was ¥297 million, FY2021 compensation was ¥206 million, and FY2020 compensation was ¥137 million.

- Comparison of Yoshiyuki Abe’s compensation growth vs BayCurrent’s revenue/net income/FCF growth over past few years:

Valuation (as of 31 May 2023)

- 31 May 2023 share price of ¥5,110

- Trailing revenue per share is ¥496.47, hence PS is 10.3

- Trailing diluted EPS is ¥137.19, hence PE is 37.2

- Trailing FCF per share is ¥132.71, hence PFCF is 38.5

- Reminder that revenue growth projection for FY2029 is for CAGR of 20% from FY2024 – the valuation does not look too rich if BayCurrent is able to grow as projected

Disclaimer: The Good Investors is the personal investing blog of two simple guys who are passionate about educating Singaporeans about stock market investing. By using this Site, you specifically agree that none of the information provided constitutes financial, investment, or other professional advice. It is only intended to provide education. Speak with a professional before making important decisions about your money, your professional life, or even your personal life. We currently have no vested interest in any company mentioned. Holdings are subject to change at any time.