There’s a gap in the investing world that I think all investors should beware. It’s a gap that can be a mile (or kilometre – depending on which measurement system you prefer) wide. It’s the gap between a favourable macroeconomic trend and a company’s stock price movement.

Suppose you could go back in time to 31 January 2006, when gold was trading at US$569 per ounce. You have an accurate crystal ball and you know the price of gold would more than triple to reach US$1,900 per ounce over the next five years. Would you have wanted to invest in Newmont Corporation, one of the largest gold producing companies in the world, on 31 January 2006? If you said yes, you would have made a small loss on your Newmont investment, according to O’Higgins Asset Management.

Newmont’s experience of having its stock price not perform well even in the face of a highly favourable macroeconomic trend (the tripling in the price of gold) is not an isolated incident. It can be seen even in an entire country’s stock market.

China’s GDP (gross domestic product) grew by an astonishing 13.3% annually from US$427 billion in 1992 to US$18 trillion in 2022. But a dollar invested in the MSCI China Index – a collection of large and mid-sized companies in the country – in late-1992 would have still been roughly a dollar as of October 2022, as shown in Figure 1. Put another way, Chinese stocks stayed flat for 30 years despite a massive macroeconomic tailwind (the 13.3% annualised growth in GDP).

Figure 1; Source: Duncan Lamont

Why have the stock prices of Newmont and Chinese companies behaved the way they did? I think the reason can be traced to some sage wisdom that the great Peter Lynch once shared in a 1994 lecture (link leads to a video; see the 14:20 min mark):

“This is very magic: it’s a very magic number, easy to remember. Coca-cola is earning 30 times per share what they did 32 years ago; the stock has gone up 30 fold. Bethlehem Steel is earning less than they did 30 years ago – the stock is half its price 30 years ago.”

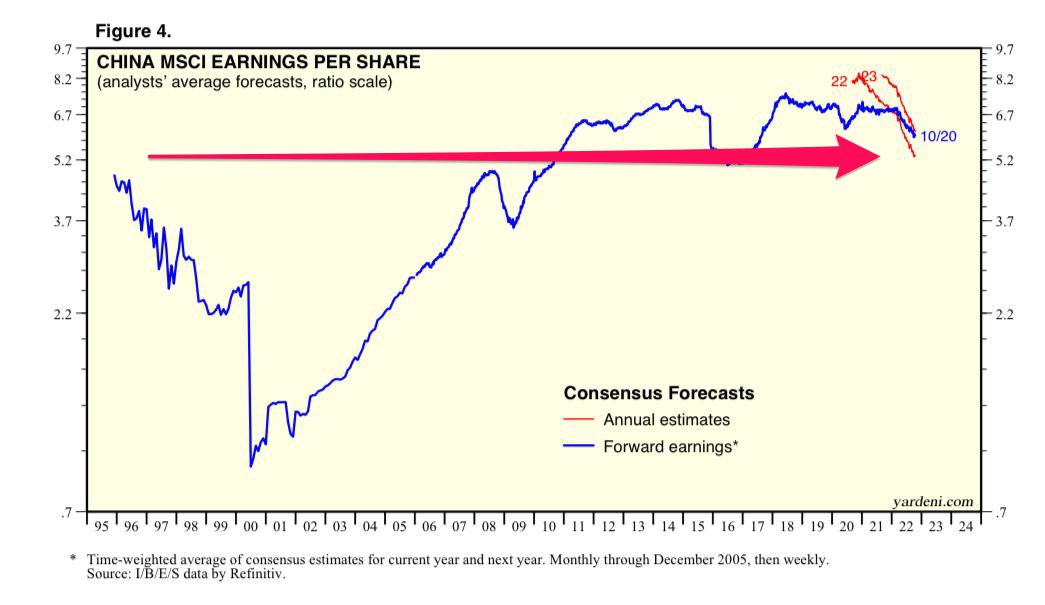

It turns out that Newmont’s net income attributable to shareholders was US$1.15 billion in 2006; in 2011, it was US$972 million, a noticeable decline. As for China’s stocks, Figure 2 below shows that the earnings per share of the MSCI China Index was basically flat from 1995 to 2021.

Figure 2; Source: Eugene Ng

There can be a massive gap between a favourable macroeconomic trend and a company’s stock price movement. The gap exists because there can be a huge difference between a company’s business performance and the trend – and what ultimately matters to a company’s stock price, is its business performance. Always mind the gap when you’re thinking about investing in a company simply because it’s enjoying some favourable macroeconomic trend.

Disclaimer: The Good Investors is the personal investing blog of two simple guys who are passionate about educating Singaporeans about stock market investing. By using this Site, you specifically agree that none of the information provided constitutes financial, investment, or other professional advice. It is only intended to provide education. Speak with a professional before making important decisions about your money, your professional life, or even your personal life. I currently have no vested interest in any companies mentioned. Holdings are subject to change at any time.