Yesterday, a wise and kind lady whom Jeremy and I know asked us: “Buying when there is blood on the street is a golden rule in investing. So should I buy Mapletree North Asia Commercial Trust now?”

I responded to her query, and I thought my answer is worth sharing with a wider audience. But first, we need a brief introduction of the stock in question.

The background

Mapletree North Asia Commercial Trust is a REIT (real estate investment trust) that is listed in Singapore’s stock market. It currently has a S$7.7 billion portfolio that holds nine properties across Beijing, Shanghai, Hong Kong, and Japan.

Festival Walk is a retail mall and is the REIT’s only property in Hong Kong. It also happens to be Mapletree North Asia Commercial Trust’s most important property. In the first half of FY19/20 (the fiscal year ending 31 March 2020), Festival Walk accounted for 62% of the REIT’s total net property income.

Hong Kong has been plagued by political and social unrest for months. On 12 November 2019, protestors in the special administrative region caused extensive damage to Festival Walk. Mapletree North Asia Commercial Trust’s share price (technically a unit price, but let’s not split hairs here!) promptly fell 4.9% to S$1.16 the day after. At S$1.16, the REIT’s share price had fallen by nearly 20% from this year’s peak of S$1.43 (after adjusting for dividends) that was reached in July.

For context on Mapletree North Asia Commercial Trust’s sliding share price over the past few months, consider two things.

First, the other REITs under the Mapletree umbrella have seen their share prices rise since Mapletree North Asia Commercial Trust’s share price peaked in July this year – the share prices of Mapletree Industrial Trust, Mapletree Logistics Trust, and Mapletree Commercial Trust have risen by 13%, 5%, and 12%, respectively (all after adjusting for dividends). Second, Mapletree North Asia Commercial Trust’s results for the second quarter of FY19/20 was released on 25 October 2019 and it was decent. Net property income was up 1.3% from a year ago while distribution per unit inched up by 0.6%. And yet, the share price has been falling.

To me, it seems obvious that fears over the unrest in Hong Kong have affected investors’ sentiment towards the REIT.

The response

My answer to the lady’s question is given in whole below (it’s lightly edited for readability, since the original message was sent as a text):

“Buying decisions should always be made in the context of a portfolio. Will a portfolio that already has 50% of its capital invested in stocks that are directly linked to Hong Kong’s economy (not just stocks listed in Hong Kong) need Mapletree North Asia Commercial Trust? I’m not sure. But in a portfolio that has very light exposure to Hong Kong, the picture changes.

Mapletree, as a group, has run all its REITs really well. But most of the public-listed REITs are well-diversified in terms of property-count or geography, or both. Mapletree North Asia Commercial Trust at its listing, and even today, is quite different – it’s very concentrated in geography and property-count. But still, the properties seem to be of high quality, so that’s good.

Buying when there’s blood on the streets makes a lot of sense. But statistics also show that of all stocks ever listed in the US from 1980 to 2014, 40% have fallen by at least 70% from their peak and never recovered. So buying when there’s blood on the streets needs a caveat: That the stock itself is not overvalued, and that the business itself still has a bright future.

Mapletree North Asia Commercial Trust’s valuation looks good, but its future will have to depend on the stability of Hong Kong 5-10 years from now. I’m optimistic about the situation in Hong Kong while recognising the short-term pain. At the same time, I won’t claim to be an expert in international relations or the socio-economic fabric of Hong Kong. So, diversification at the portfolio level will be important.

With all this being said, I think Mapletree North Asia Commercial Trust is interesting with a 2% to 3% weighting in a portfolio that does not already have a high concentration (say 20%?) of companies that do business in Hong Kong.”

Perspectives

I mentioned earlier that Mapletree North Asia Commercial Trust’s valuation looks good and that it owns high-quality properties.

The chart below shows the REIT’s dividend yield and price-to-book (PB) ratio over the last five years. Right now, the PB ratio is near a five-year low, while the dividend yield – which is nearly 7% – looks favourable compared to history.

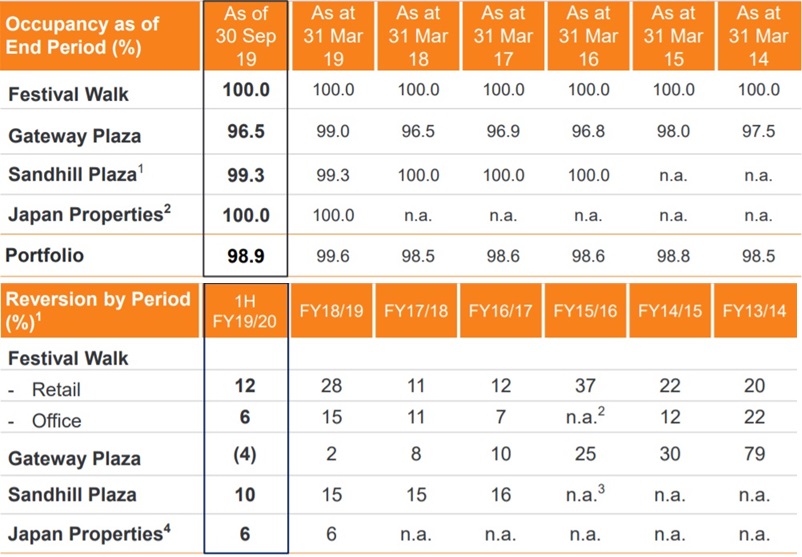

On the quality of the REIT’s property portfolio, there are two key points to make: First, the portfolio has commanded a high occupancy rate of not less than 98.5% in each of the last six fiscal years; second, the properties in the portfolio have achieved healthy rental reversion rates over the same period.

Mapletree North Asia Commercial Trust also scores well at some of the other traits that could point us to good REITs:

- Growth in gross revenue, net property income, and distribution per unit – The REIT’s net property income has grown in each year from FY14/15 to FY18/19, and has increased by 9.4% per year. Distribution per unit also climbed in each year for the same period, and was up by 4.1% annually.

- Low leverage and a strong ability to service interest payments on debt – The REIT has a high leverage ratio. As of 30 September 2019, the leverage ratio is 37.1%, which is only a small distance from the regulatory leverage ratio ceiling of 45%. But its interest cover ratio for the quarter ended 30 September 2019 is 4.2, which is fairly safe.

- Favourable lease structures and/or a long track record of growing rent on a per-area basis – At the end of FY18/19, nearly all of Festival Walk’s leases included step-up clauses in base rent. Small portions of the respective leases for the other properties in the REIT’s portfolio also contain step-up clauses. In addition, the REIT has been able to produce strong rental reversions over a multi-year period, as mentioned earlier.

Conclusion

Mapletree North Asia Commercial Trust currently has an attractive valuation in relation to history. It’s also cheaper than many other REITs in Singapore – for example, its sister REITs under the Mapletree group have dividend yields ranging from only 4% to 5%. It also has other attractive traits, such as a strong history of growth, a safe interest cover ratio, and favourable lease structures.

On the other hand, Mapletree North Asia Commercial Trust has high concentration risk since Festival Walk accounts for more than half its revenue. Moreover, Festival Walk’s prospects depend heavily on the stability of Hong Kong’s sociopolitical fabric. I don’t think anyone can be certain about Hong Kong’s future given the current unrest (which seems to have escalated in recent weeks). These increase the risk profile for the REIT in my view.

To balance both sides of the equation on Mapletree North Asia Commercial Trust, I think my point on portfolio-level diversification given in my answer to the lady’s question is critical.

I’m often asked if a certain stock is a good or bad buy. The question is deceptively difficult to answer because it depends on your risk appetite and your investment portfolio’s composition. A stock that makes sense for one portfolio may not make sense for another. Keep this in mind when you’re assessing whether Mapletree North Asia Commercial Trust is suitable for your portfolio.

Disclaimer: The Good Investors is the personal investing blog of two simple guys who are passionate about educating Singaporeans about stock market investing. By using this Site, you specifically agree that none of the information provided constitutes financial, investment, or other professional advice. It is only intended to provide education. Speak with a professional before making important decisions about your money, your professional life, or even your personal life.